Mortgage Investment Corporation Fundamentals Explained

Mortgage Investment Corporation Fundamentals Explained

Blog Article

The 2-Minute Rule for Mortgage Investment Corporation

Table of ContentsThe Single Strategy To Use For Mortgage Investment Corporation5 Simple Techniques For Mortgage Investment CorporationMortgage Investment Corporation for DummiesThe Single Strategy To Use For Mortgage Investment CorporationThe Facts About Mortgage Investment Corporation Uncovered

Does the MICs credit board evaluation each mortgage? In most scenarios, home mortgage brokers handle MICs. The broker should not serve as a participant of the credit score committee, as this puts him/her in a straight dispute of interest given that brokers typically earn a commission for placing the mortgages. 3. Do the supervisors, participants of debt board and fund manager have their own funds spent? Although an indeed to this question does not provide a safe investment, it should give some boosted protection if analyzed along with other sensible financing policies.Is the MIC levered? The financial organization will approve certain home loans had by the MIC as protection for a line of credit report.

It is important that an accounting professional conversant with MICs prepare these statements. Thank you Mr. Shewan & Mr.

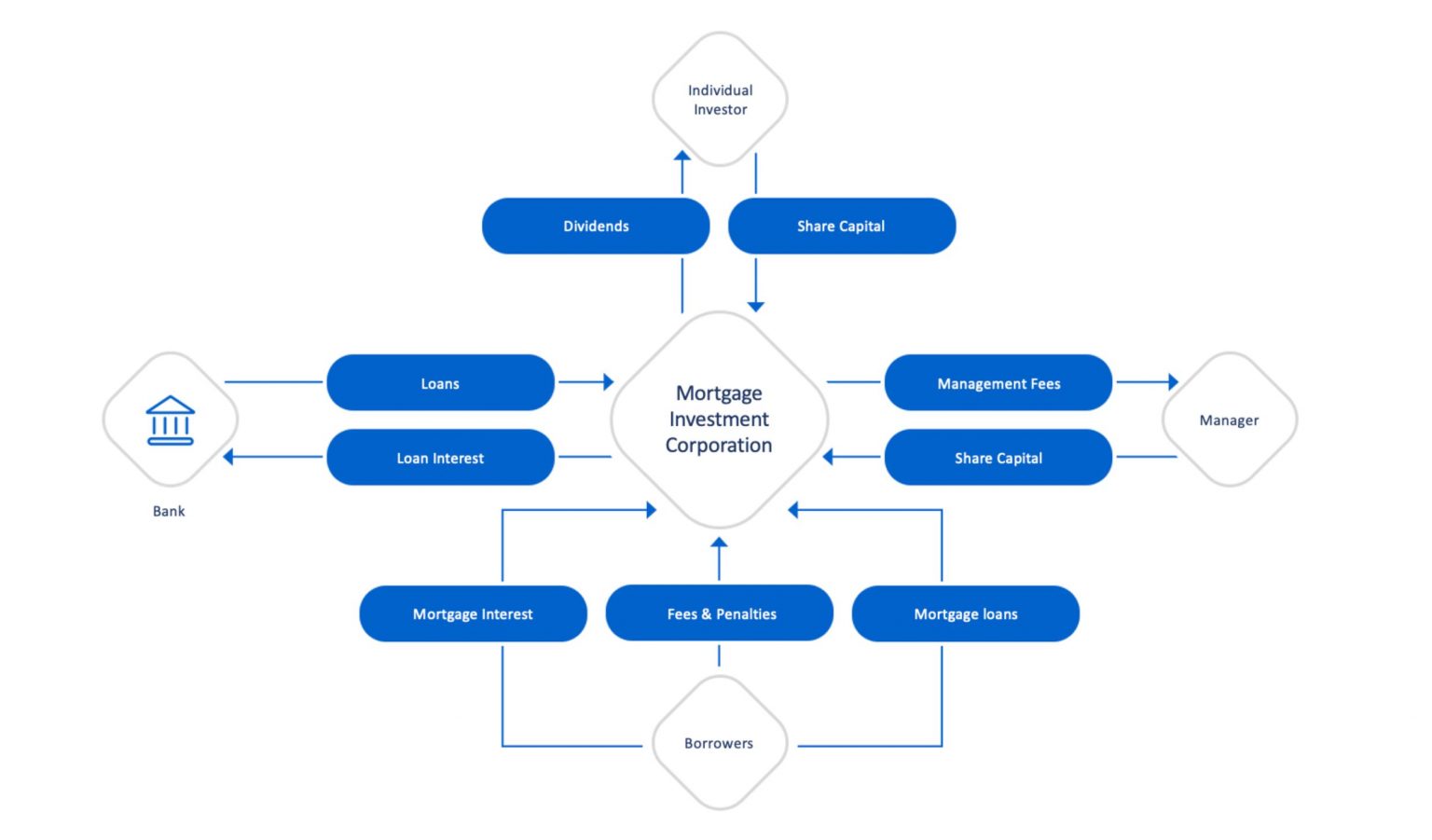

Last updated: Nov - Mortgage Investment Corporation. 14, 2018 Few investments are as advantageous as helpful Mortgage Investment Home loan Financial InvestmentCompany), when it comes to returns and tax benefitsTax obligation Since of their company structure, MICs do not pay revenue tax and are legitimately mandated to distribute all of their revenues to financiers.

This does not suggest there are not dangers, but, normally talking, whatever the more comprehensive stock market is doing, the Canadian actual estate market, particularly significant municipal areas like Toronto, Vancouver, and Montreal executes well. A MIC is a corporation developed under the rules lay out in the Revenue Tax Act, Section 130.1.

The MIC makes revenue from those home loans on passion charges and general charges. The real charm of a Home mortgage Investment Corporation is the yield it gives investors contrasted to various other set income investments. You will have no problem locating a GIC that pays 2% for a 1 year term, as government bonds are equally as low.

An Unbiased View of Mortgage Investment Corporation

There are strict requirements under the Income Tax Act that a corporation have to fulfill prior to it qualifies as a MIC. A MIC should be a Canadian company and it should invest its funds in mortgages. MICs are not allowed to manage or develop real estate residential or commercial property. That said, there click here to read are times when the MIC finishes up possessing the mortgaged building as a result of foreclosure, sale agreement, and so on.

A MIC will gain interest revenue from home loans and any cash the MIC has in the bank. As long as 100% of the profits/dividends are provided to shareholders, the MIC does not pay any type of income tax obligation. Rather than the MIC paying tax obligation on the passion it gains, investors are in charge of any type of tax check my source obligation.

Indicators on Mortgage Investment Corporation You Should Know

And Deferred Plans do not pay any kind of tax obligation on the rate of interest they are approximated to get - Mortgage Investment Corporation. That claimed, those that hold TFSAs and annuitants of RRSPs or RRIFs may be hit with specific fine taxes if the investment in the MIC is taken into consideration to be a "restricted investment" according to Canada's tax obligation code

They will guarantee you have actually located a Mortgage Financial investment Corporation with "competent investment" status. If the MIC certifies, it could be very helpful come tax time because the MIC does not pay tax obligation on the interest earnings and neither does the Deferred Strategy. Much more extensively, if the MIC falls short to meet the needs set out by the Income Tax Obligation Act, the MICs earnings will be exhausted before it gets dispersed to shareholders, decreasing returns dramatically.

It appears both the genuine estate and stock markets in Canada are at all time highs Meanwhile yields on bonds and GICs are still near record lows. Even money is shedding its allure because power and food costs have actually pushed the rising cost of living rate to a multi-year high.

The Mortgage Investment Corporation Ideas

Many tough functioning Canadians that wish to get a house can not obtain home mortgages from conventional banks because perhaps they're self used, or don't have an established credit report yet. Or perhaps they desire a brief term lending to create a large building or make some renovations. Banks have a tendency to neglect these possible borrowers since self utilized Canadians do not have steady earnings.

Report this page